Faron Pharmaceuticals — Rights Issue Commences

Rose Garden Capital presents previously undisclosed information on investigations concerning Faron and examines the details of the ongoing rights issue.

Faron Pharmaceuticals is a Nordic biotechnology company listed on First North Helsinki and the AIM market in London. The company develops immuno-oncology therapies, with bexmarilimab as its lead asset, and is preparing to advance the program into Phase II and Phase III development. Faron is currently undertaking a share issue.

This article provides background on the investigations concerning Faron by the Finnish Financial Supervisory Authority. In addition, it evaluates the rights issue from a financial perspective.

The article is divided into five chapters as follows:

Chapter 1. The Investigations

Chapter 2. The Rights Issue

Chapter 3. Comparison to the 2024 Open Offer

Chapter 4. Rights Issue Terms

Chapter 5. Closing Remarks

Chapter 1. The Investigations

In connection with the 2026 Rights Offering, which is discussed further in Chapters 2, 3 and 4, Faron disclosed that the Disciplinary Committee of Nasdaq Helsinki had initiated proceedings concerning the company. However, Faron has also been subject to two separate cases by the Finnish Financial Supervisory Authority (FIN-FSA). Faron has not disclosed these latter cases to the market and disclosed the Disciplinary Committee proceeding only in the prospectus relating to the Rights Issue, which was approved by the FIN-FSA. This chapter sets out the information that, in our view, should be made known to the public and offers more information on the Disciplinary Committee proceeding.

Nasdaq Helsinki Issue

Faron’s common stock is traded on the First North Growth Market Finland operated by Nasdaq Helsinki, which is subject to the supervision of the Finnish Financial Supervisory Authority. Nasdaq Helsinki Surveillance is responsible for monitoring whether issuers listed on the marketplace comply with the applicable rules and regulations. The Surveillance function may initiate an investigation if it determines that a company may have breached those rules. If an investigation results in the conclusion that a company has violated the rules and the company is unable to provide an acceptable explanation for its conduct, the Surveillance function may issue a non-public reprimand. However, if the breach is considered material and the explanation inadequate, the matter may be referred to the Disciplinary Committee.

The Disciplinary Committee is an independent body. It may base its decision on the material gathered during the Surveillance investigation, but it may also request additional evidence from the company concerned. If the Disciplinary Committee decides to impose a sanction, the sanction may range from a warning to delisting.

It remains unclear which specific incident or disclosure the proceedings concerning Faron relate to, but the company has stated that the matter concerns allegedly misleading information presented in an interview and the adequacy of its corporate governance arrangements. We have repeatedly noted that certain public comments have appeared materially disconnected from the underlying facts. For further discussion, please refer to our earlier articles on Faron Pharmaceuticals published at rosegarden.capital.

The matter has already been referred to the Disciplinary Committee and, accordingly, there is a meaningful possibility that the Committee will impose a sanction. The Committee’s decision is final and not subject to appeal. In our assessment, the most likely outcome is a monetary fine. The potential range of such a fine is not specified in the First North Helsinki rulebook. However, on the main market, fines range from €10,000 to €500,000, and we believe any potential fine would likely fall within a comparable range. The financial significance of a possible sanction is therefore limited. Nevertheless, the matter highlights that the company’s public statements may at times be misaligned with the underlying circumstances and should therefore be interpreted with particular caution. A decision, together with the publication of further details, is expected in spring 2026.

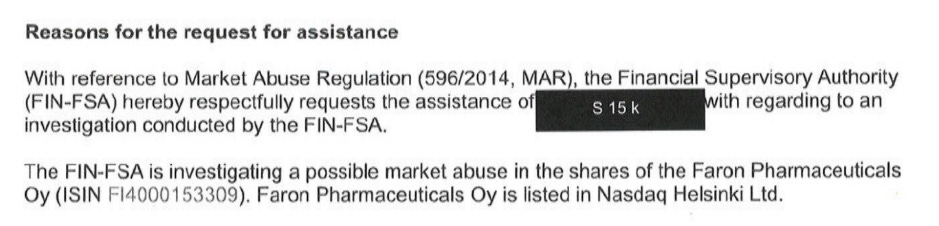

Finnish Financial Supervisory Authority Case No. 1

Faron has been involved in two FIN-FSA cases, both of which appear to remain ongoing. The first is an investigation concerning possible market abuse in Faron’s shares. The suspected conduct appears to be connected to the public share issue carried out in 2024.

The details of the investigation are not publicly available, as the matter remains ongoing and the latest known developments date to early 2026. Based on the information available to us, the matter concerns the alleged misuse of inside information, which is prohibited under Chapter 51, Sections 1 and 2 of the Finnish Penal Code. A party found guilty may be subject to a fine or a term of imprisonment of up to four years.

It is not known who is the subject of the investigation. We therefore refrain from making conjectures regarding the party concerned or the implications of the matter for the company and the ongoing rights issue.

The misuse of inside information constitutes a serious violation of market integrity. It disadvantages ordinary investors who do not have access to non-public information. As a result, such conduct may reduce returns for law-abiding investors, increase transaction costs, and impair the overall efficiency and credibility of financial markets.

Finnish Financial Supervisory Authority Case No. 2

The second case dates back to late 2025 and, based on the information available to us, appears to remain ongoing. In this matter, the FIN-FSA has requested clarification regarding the market sounding process conducted by Faron. Market sounding refers to the process of assessing potential investors’ interest in a contemplated transaction and the terms associated with it. It is typically conducted in advance of transactions such as share issues in order to support the appropriate structuring of the terms. Market sounding is subject to extensive regulation under the EU Market Abuse Regulation (MAR).

You may expect further details in forthcoming articles. Please consider subscribing to be among the first to gain access. Subscribing is free, and we guarantee not to present any advertisements or employ any paywalls.

Chapter 2. The Rights Issue

On 9 February, Faron announced that it is seeking to raise gross proceeds of €40 million through a rights issue. This chapter examines the rights issue and the background to the transaction.

Background

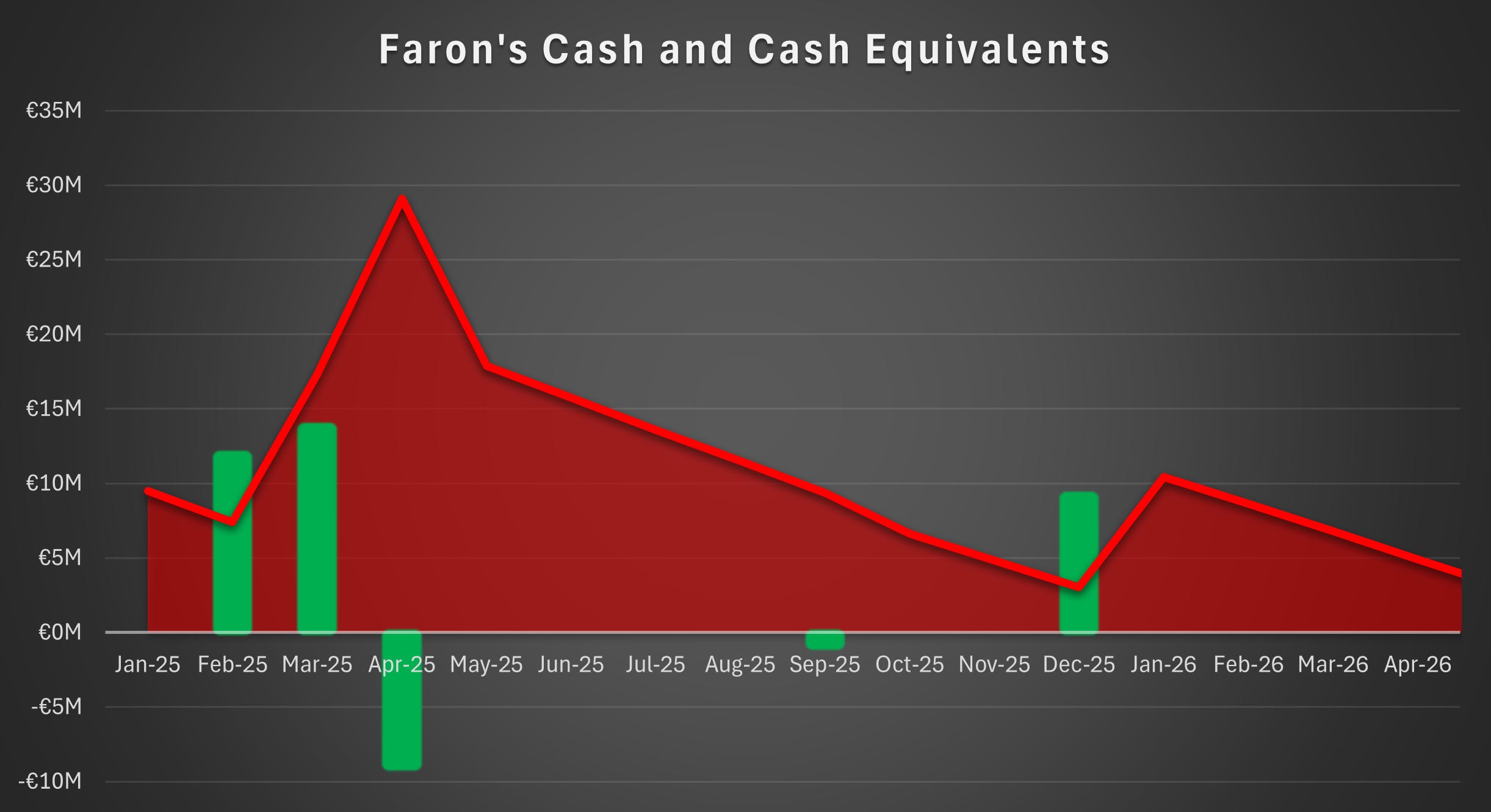

Faron’s cash position amounted to €12.3 million at year-end 2025, which was sufficient to cover its financial obligations until the second half of 2026, but insufficient to fund further clinical studies. To advance its lead asset, bexmarilimab, into Phase III development, Faron had disclosed that it was pursuing a licensing agreement under which a licensee would assume some or all of the costs of further studies and pay the licensor royalties, an upfront payment, and milestone payments in exchange for the commercial rights to the drug.

We have long argued that such a licensing agreement was unlikely to materialize for several reasons. For further discussion of the matter, please refer to our earlier article here. In particular, the predatory financing arrangement with Heights Capital Management (HCM) materially weakened Faron’s negotiating position. For further analysis of the HCM financing arrangement, please refer to our earlier articles at rosegarden.capital.

Chief Executive Officer Dr. Jalkanen has argued that the reason such a partnership did not materialize was the failure of a competitor’s trial. From an external perspective, it is difficult to assess the accuracy of Dr. Jalkanen’s comments, but they appear unconvincing. The share price has declined by more than 70% since the company announced the rights issue, which suggests that virtually any alternative non-dilutive arrangement, such as a licensing agreement, would likely have been in the best interests of shareholders. In our view, the chosen course of action has most likely reflected the company’s weak negotiating position and the misalignment between management’s interests and those of shareholders. Faron is effectively a family-controlled business, which suggests that its primary objective is not necessarily the maximization of shareholder value, but rather the independent advancement of a potential cancer treatment discovered by the family.

Impact on the Pipeline

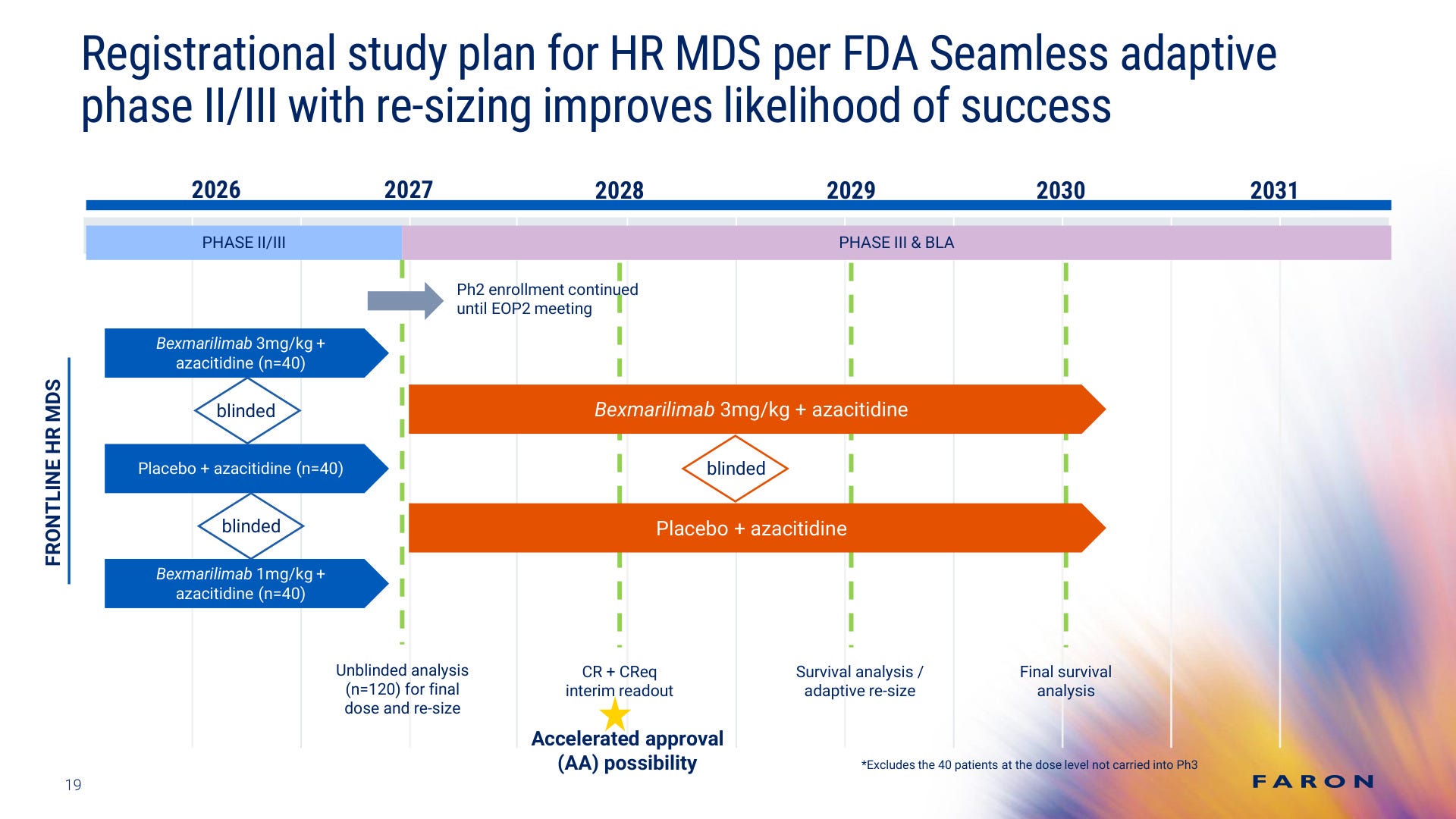

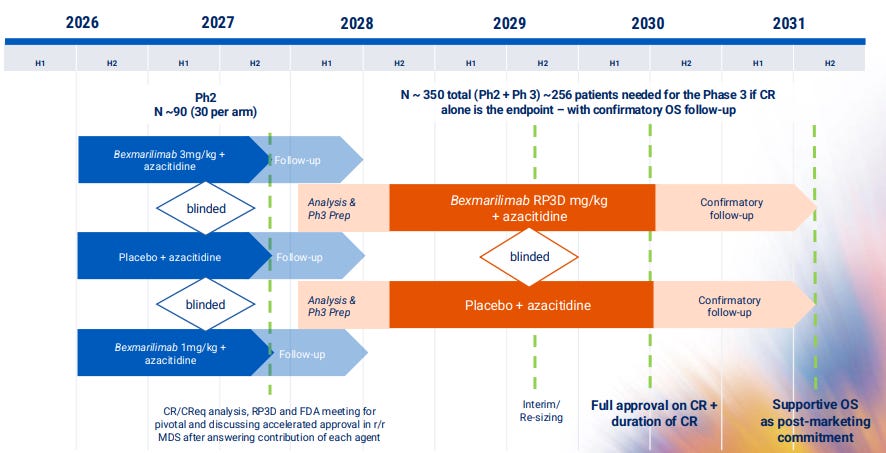

Due to the absence of a partner, the company cannot afford to conduct the extensive Phase II/III study it had previously envisaged.

In order to reduce costs, the company has opted for a separate blinded Phase II study with a more limited patient population. Contingent on strong results, such a trial could enable the company to out-license the project before Phase III. We have long argued that a controlled randomized trial is effectively a prerequisite for a licensing transaction with a large pharmaceutical company. Accordingly, the successful completion of the planned trial could enable Faron to out-license the project following the readout.

The company expects to commence the study in the second half of 2026. The timeline, especially the timing of the readout, appears ambitious in our view.

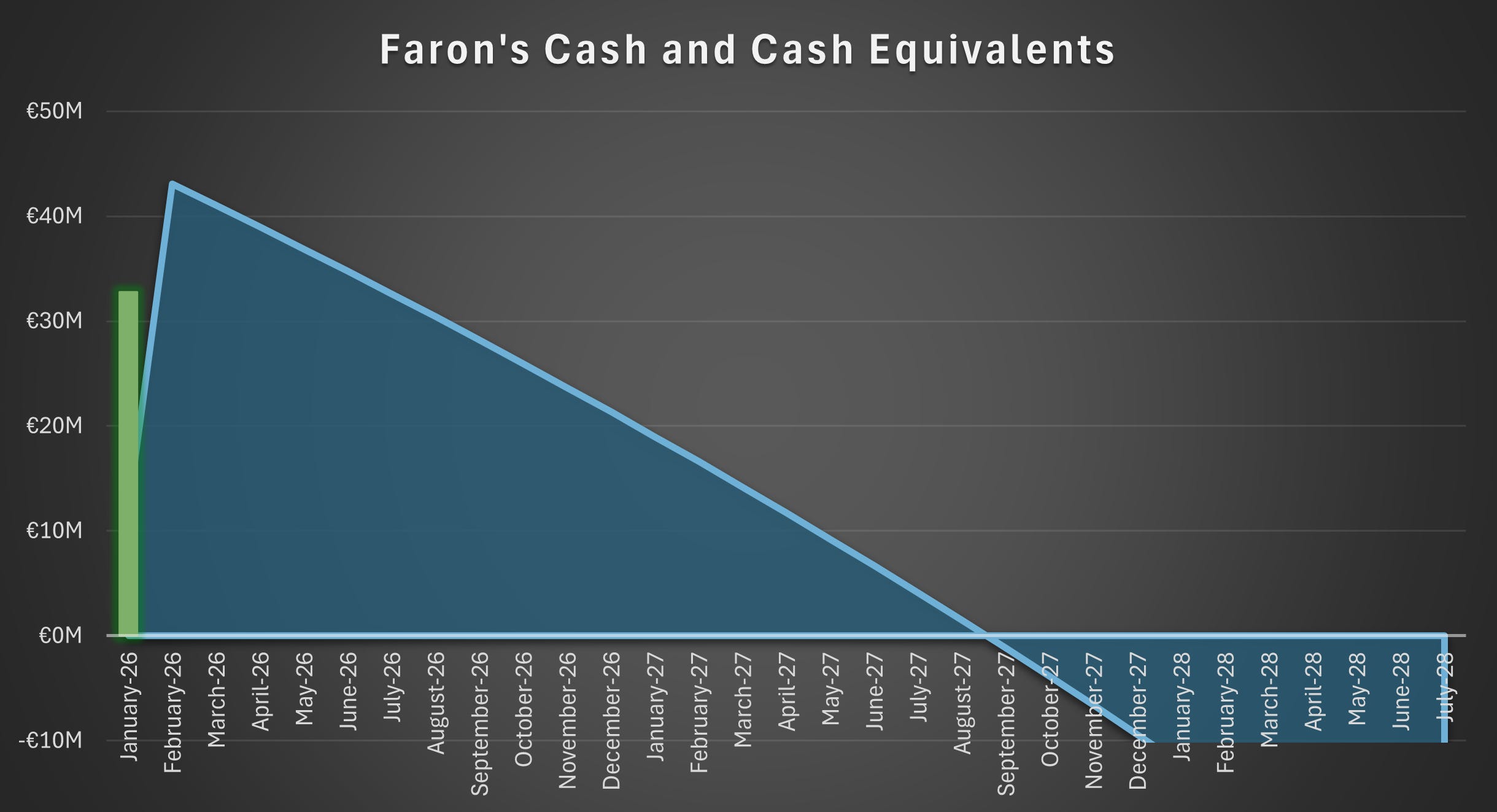

The rights issue is fully secured. Accordingly, the company’s operational pathway remains unchanged regardless of the subscription rate. However, the proceeds are not sufficient to fund the company through the trial readout, whether that occurs in the latter part of the second half of 2027 or, as we consider more likely, at a later date.

Runway

The rights issue will provide the company with gross proceeds of €40.1 million and net proceeds of €32.8 million. These proceeds are sufficient to fund the company until the second half of 2027.

The company addresses this funding horizon by indicating the possibility of further directed share issues under the existing authorization granted at the 2025 annual general meeting, or AGM. In addition, as the company will hold its 2026 AGM in May, we expect the board to propose a further authorization for the issuance of approximately 50 million new shares. This authorization would likely be required primarily to facilitate the issuance of additional shares and special rights in connection with the HCM arrangement, under which the current amount of special rights appears insufficient in light of the significantly lower share price. Moreover, the company’s option program is likely to require adjustment as a result of dilution.

The remaining authorization for 19 million shares granted at the 2025 AGM remains available until 30 June 2026. Should the company fail to attract investor interest in a directed share issue before that date, a broader authorization would likely be necessary. In our view, a directed issue would be superior compared to another rights issue prior to the readout.

The company has not introduced any cost reduction measures in connection with the rights issue. In our view, management should consider reducing costs wherever possible, given the apparently high cost of raising capital through both equity offerings and debt financing.

Timeline

The subscription period runs until 2 April on First North Helsinki and until 31 May on the AIM market in London. The final result of the rights issue will be announced on 9 April, after which the guarantors will be allocated their respective shares.

Chapter 3. Comparison with the 2024 Open Offer

In 2024, Faron was in a broadly similar position, with a cash balance insufficient to finance Phase II clinical studies. This chapter compares the 2024 open offer with the 2026 rights issue across relevant dimensions, including valuation.

Difference Between an Open Offer and a Rights Issue

From a technical perspective, an open offer and a rights issue differ fundamentally. An open offer transfers value from existing shareholders to new investors if the offer price is below the market price. By contrast, a rights issue has no effect on equity value attributable to each share if transaction costs are disregarded. This holds irrespective of whether an investor is willing to commit additional capital, provided that the subscription rights are tradable.

In practice, however, the share price often declines toward the offer price, which renders the subscription rights largely worthless. One possible explanation is that subscription rights or subscription options require cash to be exercised, which can influence market dynamics in actual trading conditions. At the same time, rights issues are rarely independent of underlying business developments. In Faron’s case, the announcement of the rights issue ultimately made it clear that a licensing transaction was unattainable.

Comparing the Financial Position

Notably, Faron’s position with respect to the path toward market approval remains broadly similar. In 2024, BEXMAB02 was considered to be the study preceding a registrational Phase III trial. The upcoming Phase II study is now expected to serve a similar role. Accordingly, the estimated time to potential approval is broadly comparable, which allows for a meaningful like-for-like comparison. Moreover, the target market remains broadly similar, especially after taking into account the substantial uncertainty inherent in forecasting drug sales.

The more significant differences relate to the capital structure and the contingent claims on Faron’s equity, most notably its debt financing instruments. In 2024, Faron had an outstanding loan from IPF Partners. The loan was amortized through cash payments, but it was also the principal reason for the 2024 open offer, as the indenture required cash covenants that Faron ultimately breached. In early 2025, the loan was repaid using proceeds from the HCM loan agreement, which has been discussed extensively in our earlier articles available at rosegarden.capital. The early repayment of the IPF loan resulted in early repayment fees of €1.1 million, while the warrants issued to IPF as a sweetener remained outstanding. The terms of the HCM loan are highly predatory and are typically encountered only in financially distressed companies. Accordingly, the underlying rationale for the switch to HCM remains unclear, but the implications for investors have now become fully apparent. As of 18 March 2026, the remaining principal amount of the HCM bonds was €17.1 million and their fair value was €23 million following the conversion price reset.

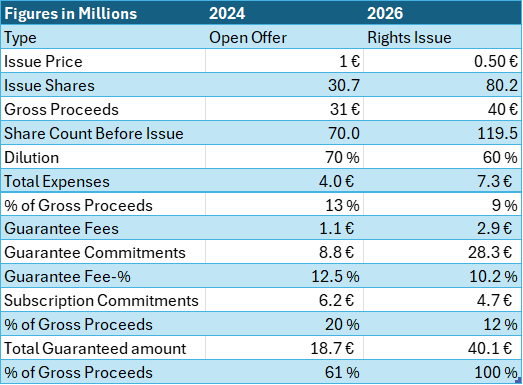

Comparing the Offers

The key parameters of the two offerings are set out below. Guarantee commitments are fee-based commitments, typically provided by external investors. Subscription commitments are unpaid commitments and are typically provided by existing shareholders. In addition to the guarantee and subscription commitments listed below for the 2026 Rights Issue, the transaction also includes cornerstone investments amounting to €4.7 million.

Most notably, the offer price has halved. In practical terms, this indicates that the company has been unable to generate shareholder value over the past two years.

Moreover, the costs associated with the rights issue are materially higher. In 2024, a rights issue was considered, but it proved infeasible due to time constraints. In the current situation, there is no comparable immediate timing pressure, which has enabled the company to pursue a more expensive and time-consuming rights issue instead. Although issue-related costs have increased from €2.9 million to €4.4 million, we consider the rights issue to be a fairer alternative for shareholders.

Possibly due to the financing pressure and time constraints that were evident in 2024, the company was able to secure only a limited number of underwriters. In 2026, by contrast, the company has fully secured the issue, thereby eliminating execution risk related to the outcome.

Subscription commitments are lower than in 2024. The principal reason is that the company’s largest shareholder, Mr. Syrjälä, has not indicated an intention to subscribe for his pro rata share. The subscription commitments relating to the 2026 rights issue are discussed in greater detail in Chapter 4.

Market Terms

The theoretical ex-rights price (TERP) for the 2024 issue amounted to €1.95. Accordingly, the issue price of €1 implied a discount of 49% to TERP. However, in both the 2024 open offer and the 2026 rights issue, the offer announcement contained a substantial amount of additional information, both implicitly and explicitly, that affected expectations regarding future cash flows. TERP should therefore be interpreted as an illustrative measure.

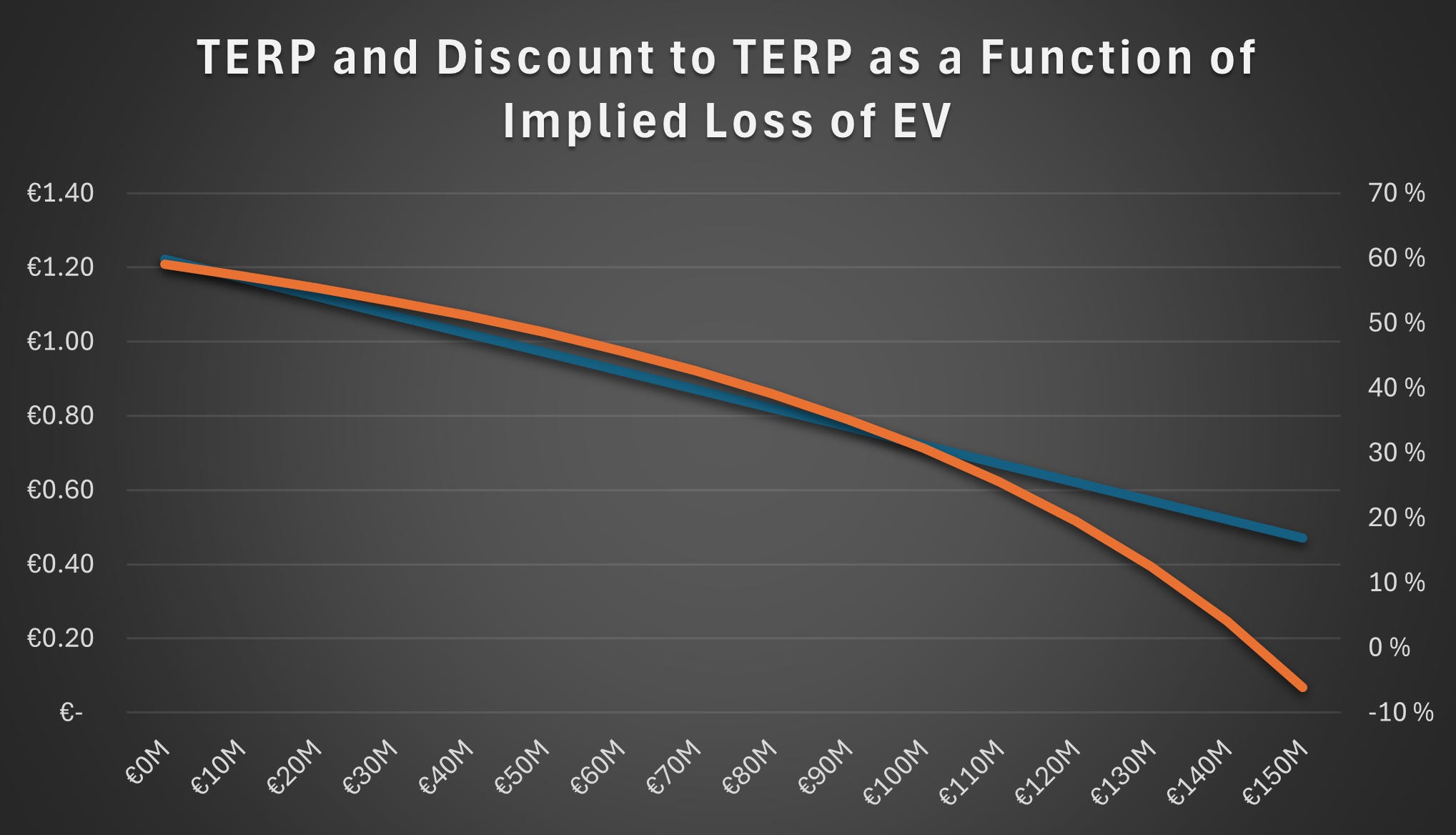

Similarly, in the 2026 rights issue, the preceding share price was €1.80, corresponding to a TERP of €1.22 and a discount to TERP of 59%. These figures reflect transaction expenses and the increase in the valuation of the outstanding warrants and convertible instruments. However, to derive a more economically meaningful TERP, one must also estimate the decline in Enterprise Value (EV) resulting from the delay, the revised trial plans, and the reduced likelihood of a licensing agreement.

Figure 6 shows TERP and the discount to TERP on the right axis as a function of the implied loss in enterprise value (EV). If the implied loss is assumed to exceed €144 million, the offering would be priced at a premium to TERP.

For a more accurate comparison, it is useful to examine the pre-money and post-money market valuations of both market capitalization and enterprise value.

For the 2024 open offer, the pre-money market capitalization amounted to €70 million and enterprise value to €60 million. For the 2026 Rights Issue, the pre-money market capitalization at the issue price is €60 million. This corresponds to an enterprise value of €72 million when the convertible instruments are measured at fair value. In broad terms, the two offerings are priced at broadly similar levels.

Chapter 4. Rights Issue Terms

This chapter examines the terms of the rights issue.

Subscription and Anchor Commitments

The rights issue is fully covered through subscription commitments, anchor commitments, and guarantee commitments.

Most notably, the company’s largest shareholder, Mr. Syrjälä, has not committed to subscribing for his pro rata share. As a result, his ownership interest in the company will be materially diluted unless he subscribes for an amount exceeding his existing commitment. We consider that outcome unlikely. Had he intended to subscribe for a meaningful allocation, he could have provided such a commitment, thereby reducing the cash compensation payable to external guarantors and effectively supporting the value of his existing ownership interest. Alternatively, he could have provided a subscription guarantee in exchange for a fee.

Commitments from Faron’s board and management team are limited. Only the Chair of the Board, Mr. Pätsi, has provided subscription commitments and anchor commitments.

In addition, Ms. Jalkanen, the co-founder of the company, has committed to subscribing for 100,000 shares, which is materially below her respective pro rata share.

No executives have indicated an intention to subscribe for shares.

In addition to subscription commitments, several new investors have expressed an interest in subscribing for shares through anchor commitments totaling €7 million. The distinction between subscription commitments and anchor commitments is that anchor commitments are used to subscribe for shares that would otherwise remain unsubscribed and are therefore allocated without subscription rights.

Guarantee Commitments

After taking into account the anchor commitments and subscription commitments, the remaining 70.65% of the rights issue is covered by guarantee commitments. A total fee of €2.9 million will be paid to the guarantors, implying an average guarantee fee of approximately 10%. However, we believe that HCM will receive a fee of 11% in light of its role, while the other guarantors will receive 8%. The fee will be paid in cash.

Below, we introduce the guarantors and provide an assessment of whether each entity should be regarded as a long-term holder or a short-term holder. We classify an investor as short term if, in our view, it is likely to divest any allocated shares within 0 to 6 months. Investors that do not fall within this category are classified as long term.

HCM

Commitment: 39 million shares

In addition to the convertible bonds, HCM has committed to subscribe for a substantial number of shares. Owing to the predatory nature of the loan agreement, HCM effectively has decisive influence over Faron’s financing alternatives. HCM is largely insulated from changes in Faron’s share price arising from equity issuances, because the conversion price is set by reference to the offering price. Accordingly, the offer price is ultimately determined by HCM. We therefore regard HCM as a short-term investor that is likely to divest any allocated shares as soon as practicable. HCM has agreed not to accelerate any convertible repayments for a period of 60 days following the rights issue. However, the guarantee commitment is not subject to transfer restrictions.

Pentwater Capital

Commitment: 6 million shares

Pentwater Capital is a hedge fund and is, in our view, likely to divest any allocation promptly after the rights issue.

Anavio Capital Partners

Commitment: 3 million shares

Anavio is an investment firm that frequently provides financing support as a guarantor and is therefore likely to divest any allocated shares rapidly.

Fenja Capital

Commitment: 2 million shares

Fenja Capital is a Swedish investment firm that frequently participates in rights issues as a guarantor and is known for liquidating its allocation promptly.

In addition, there are six further guarantors with smaller allocations, which we also consider likely to be short-term investors. Accordingly, we believe that all guarantors in the transaction are short-term investors and are therefore likely to liquidate any allocated shares within a relatively short period.

Allocation

Shares are allocated first to those who have subscribed for shares with subscription rights. Second, shares are allocated to those who have subscribed for shares both with and without subscription rights. Third, shares are allocated to those who have subscribed for shares without subscription rights. Fourth, shares are allocated to anchor investors and finally to guarantors.

Accordingly, any subscriptions made in excess of committed amounts are, in effect, allocated at the expense of the guarantors. This means that the price at which guarantors can sell their shares while still generating a profit is materially below the issue price and depends solely on the number of shares subscribed for by other investors.

Effective Issue Price for Guarantors

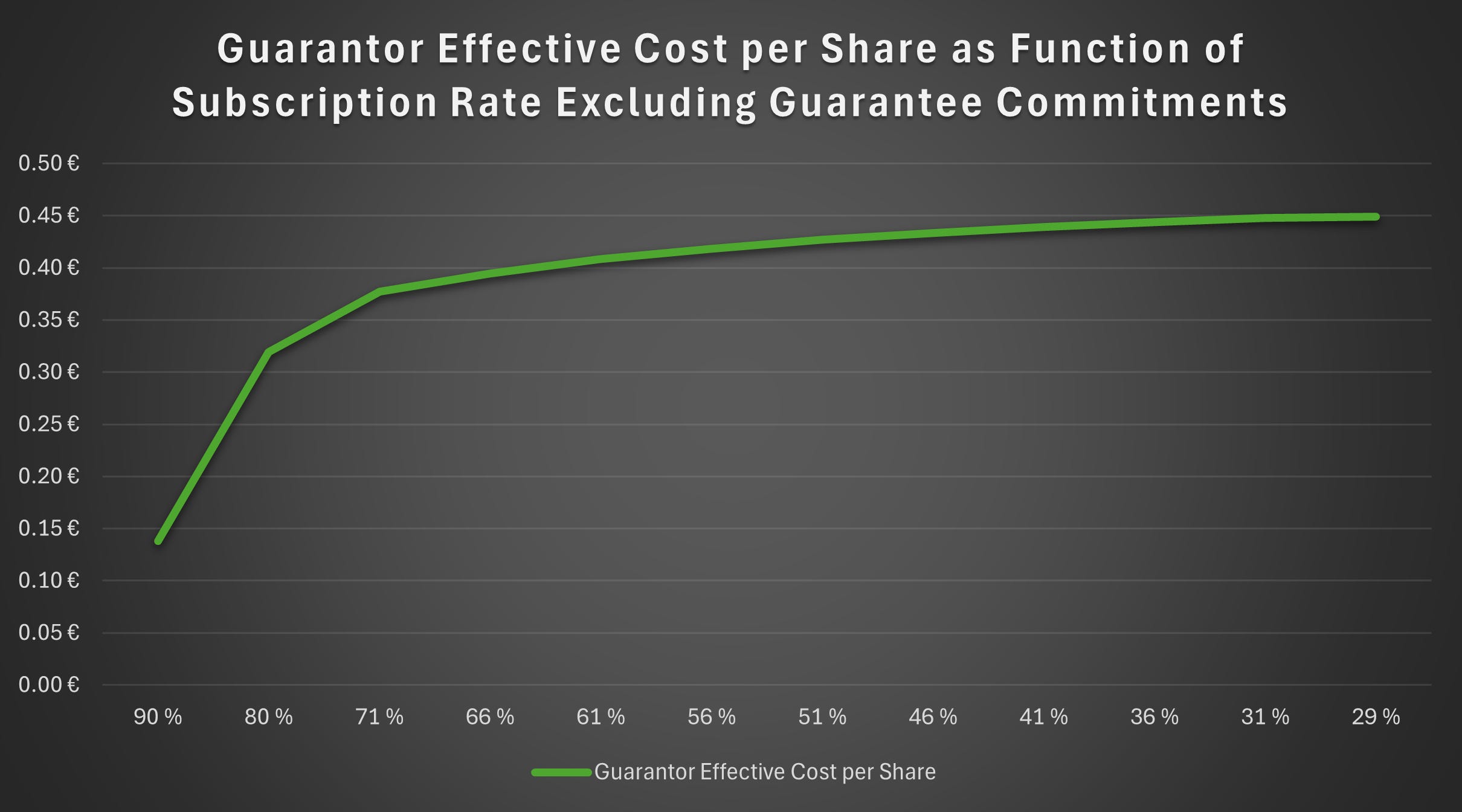

The guarantors will receive total cash compensation of €2.9 million. This compensation is payable irrespective of the number of shares ultimately allocated to them. We believe that HCM’s compensation differs from that of the other guarantors. However, the following figures are based on the simplifying assumption that compensation is distributed evenly among all guarantors.

As shown in Figure 7, the effective cost to guarantors is materially below the actual subscription price. The horizontal axis shows the subscription rate excluding guarantee commitments. Accordingly, a subscription rate of 71% refers to a scenario in which 29% of the issue is allocated to guarantors, corresponding to an allocation worth approximately €12 million. In that case, the guarantors break even provided that they are able to divest the shares at a price of €0.39 or above. If the subscription rate exceeds 71%, the effective price declines rapidly, although the actual allocation to guarantors also decreases. At the other end of the range, 29% refers to a situation in which no subscriptions are made beyond the subscription commitments and anchor commitments.

Result

We estimate that approximately 50% to 80% of the rights issue will be subscribed for, both with and without subscription rights, including the subscription commitments and anchor commitments. This would imply an allocation to guarantors of approximately 20% to 50% of the issue. On that basis, the guarantors’ effective subscription price would be approximately €0.32 to €0.43, with an allocation of roughly 16 million to 40 million shares. Accordingly, a higher overall subscription rate would imply lower selling pressure on the stock.

Chapter 5. Closing Remarks

Thank you for reading. We wish our readers continued success this spring. We also encourage you to appreciate the world and the people around you.

In forthcoming articles, we will examine the total cost of the HCM transaction for Faron and its shareholders in order to illustrate, once again, how difficult it is to recover from this type of financing error without a detrimental and dilutive equity injection. Furthermore, we will assess the outcome of the rights issue and its implications for the market. In addition, we will continue to report on developments relating to the Disciplinary Committee’s decision and the Finnish Financial Supervisory Authority’s investigation into suspected market abuse, as well as related matters.

Please consider subscribing to receive new articles by email as soon as they are released. Subscribing is free, and we guarantee not to present any advertisements or employ any paywalls.

The information presented in this blog is provided solely for educational and informational purposes and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instrument. The views expressed are those of the author and may change without notice. You should not rely on this content as the basis for making any investment decision, and nothing herein guarantees future performance of any market or security. The author is not a regulated financial advisor or any other licensed financial services provider. Prior to taking any action, you are strongly encouraged to conduct your own research and seek guidance from a qualified financial professional who can take into account your individual circumstances and risk tolerance. Although every effort is made to ensure accuracy at the time of publication, errors or omissions may occur. Always corroborate key facts with multiple reputable sources and, where feasible, trace assertions back to the original source material. References to third-party content are provided solely for convenience and do not imply endorsement, and no responsibility is assumed for their completeness, reliability, or timeliness. The topics covered are not necessarily exhaustive.